Global Markets Rebound After Historic Bloodbath, Japan Soars

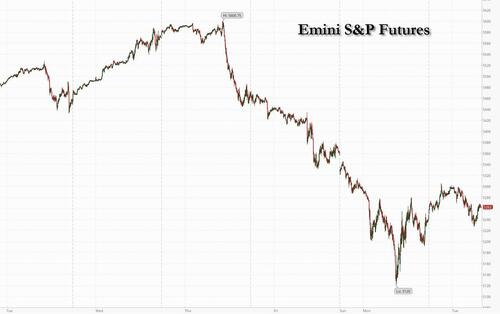

After Monday’s historic selloff that capped a three-week, $6.4 trillion rout in global equities as a brutal unwind in the carry trade driven by last week’s BOJ rate hike hammered most consensus trades, a dead cat bounce arrived as some investors looked for bargains and markets saw a hint of calm return on Tuesday, but the rebound has been decidedly more tepid than the rout, and doesn’t prove the meltdown is over. Futures on the S&P 500 and Nasdaq are poised to regain only a fraction of yesterday’s loss, while stocks in the UK and Europe gave up earlier gains to head lower. There were stronger moves in Japan, where the two key share gauges both jumped more than 9% at the close after tumbling 12% the day before. US futures higher in a volatile, shaky session, with small caps lagging the Nasdaq, as USD finds support and Japanese Equities rally 10% overnight, erasing much of Monday’s loss. As of 7:45am, S&P futures were up 0.8%, off session highs, while Nasdaq futures rebounded 1.1% falling more than 7% over past three sessions. That said, much of the overnight gains were pared after JPM’s co-head of FX Strategy Arindam Sandilya said that we may only be 50% – 60% through this carry trade unwind. Bond yields are 5-6bps higher as treasuries retreated, with the 10-year yield heading for the first increase in almost two weeks as traders curbed bets that the Federal Reserve will step in to support markets with early interest rate cuts. Commodities are weaker, with WTI and gold modestly in the green. For the remainder of the week, the macro catalysts are bond auctions and Fedspeak.

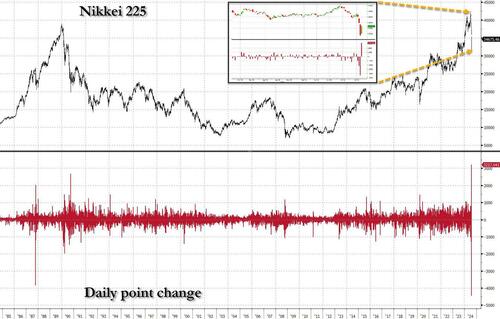

Overnight, the bulk of the action was once again in Japan, where the Nikkei 225 index surged 3,217.46 points on Tuesday – its largest single-day rise following the largest one-day drop in history – after US service sector data for July eased concerns of a recession. The average ended the day at 34,675.46, up 3,217.46 points, or 10.2%. The index’s previous biggest single-day jump dates back to October 1990, when it gained 2,676.55 points. By percent, it was the biggest increase since 2008 and the fourth-largest rise ever.

A big reason for Japan’s rebound is because of an emergency meeting between the BOJ and the MOF as Japan’s government and central bank sought to show a united front and restore calm to financial markets, after the biggest stocks plunge in more than three decades triggered criticism of monetary policy tightening and cast a shadow over efforts to get households to invest their assets. With some pointing fingers at the central bank’s decision to hike rates last week as part of the trigger for the market turmoil seen in the last few days, the government appears to be trying to show it’s standing with the BOJ remains unchanged, at least for now.

Anyway, back to the US, where in premarket trading, the Mag7 is higher with Semis up small. Alphabet (GOOGL US) edged 0.3% higher in premarket trading, as a global tech rebound allows the shares to look past Monday’s ruling by a US judge that Google illegally monopolized the search market through exclusive deals. Analysts say a modest stock move was expected, as Alphabet will appeal the verdict and the process will take time to resolve. Palantir shares are up 7.4%, after the data-analysis software company reported second-quarter results that beat expectations. It also raised its full-year forecast and touted the demand it is seeing from artificial intelligence software. Here are the other notable premarket movers:

- Apple (AAPL US) shares are largely flat in US premarket trading, as analysts note that Monday’s ruling on Google by a US judge might impact the $20B+ the iPhone maker collects annually from the search giant. The stock is fluctuating even as global tech stocks rebound on Tuesday.

- Cadence Design (CDNS US) shares rose 2.4% as Piper Sandler raised the recommendation on the software company to overweight from neutral after the recent decline in the stock.

- Celsius Holdings (CELH US) shares climb 8.1% after the energy-drink maker reported second-quarter revenue and earnings per share that topped Wall Street expectations.

- Chegg (CHGG US) shares slide 19% after the education technology company’s forecast for third-quarter adjusted Ebitda missed consensus estimates. Piper Sandler said this was a disappointing quarter from the company.

- CrowdStrike (CRWD US) rose 2.8% as Piper Sandler raised the recommendation on the cyber security company to overweight from neutral, saying investors should “opportunistically build positions at current levels.”

- Hims & Hers Health (HIMS US) shares rise 4.3% after the firm boosts full-year adjusted Ebitda guidance above the average analyst estimate. The telehealth company reported second-quarter revenue that beat estimates. Citi described the performance as “impressive,” but noted that the debate on GLP-1 weight loss drugs was far from over.

- Lucid (LCID US) shares jump 13% after the EV startup announced a commitment of as much as $1.5 billion from one of its biggest investors — an affiliate of Saudi Arabia’s Public Investment fund. Lucid also reported second-quarter revenue that beat the average analyst estimate.

- Lumen Technologies (LUMN US) shares soar 42% after the company said artificial intelligence demand has driven $5 billion of new business and that it is in talks for a further $7 billion in potential sales. Citi upgraded its rating on the stock to neutral from sell after the announcement.

- Yum China (YUMC US) shares jump 8.1%, after the fast-food chain operator’s restaurant margin held up better than expected in the second quarter despite a sluggish economy and weaker same-store sales. Analysts said the profit resilience was a result of stricter cost controls and initiatives such as staff and space sharing between neighboring restaurants.

- ZoomInfo Technologies (ZI US) shares drop 15% after the infrastructure-software company reported second-quarter results that missed expectations and cut its full-year forecast for adjusted earnings. KeyBanc Capital Markets, DA Davidson and Raymond James all downgraded their recommendations on the stock to a hold-equivalent rating.

Underscoring the broad market angst, investors are rushing to insure their portfolios against an extreme market crash. And Wall Street’s “fear gauge,” the VIX index, remains at the highest level in almost two years.

“We don’t expect a lull in the coming days,” said Christopher Dembik, senior investment adviser at Pictet Asset Management. The unraveling of the yen carry trade will continue to trigger margin calls and losses, while a sustained recovery in stocks hinges on central banks measures and big-tech earnings, he said. “I’m expecting the month of August to be red-tainted.”

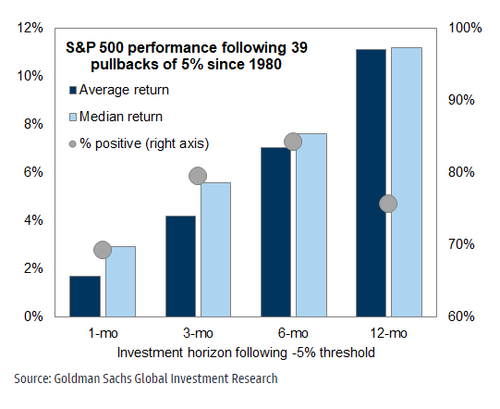

Even so, the small moves suggested some calm is returning to markets. In an attempt to awaken animal spirits, Goldman’s David Kostin said that buying the S&P 500 after a decline of 5% has usually been profitable in the past four decades. According to Kostin, investors typically profit when buying the S&P 500 index following a 5% sell-off. Since 1980, an investor buying the S&P 500 index 5% below its recent high would have generated a median return of 6% over the subsequent 3 months, enjoying a positive return in 84% of episodes.

Mohit Kumar, chief economist for Europe at Jefferies, echoed Kostin’s sentiment saying that „the violent market moves over the last few sessions, in our view, present a buying opportunity.”

European stocks started off well in the green, but the buying waned with most European bourses now flat or lower; a paring which has occurred without a fresh fundamental driver. The Stoxx 600 was down -0.2% near session lows. Tech outperforms as it rebounds with Deutsche Bank also upgrading the European sector while Banks come in a close second place as they trim recent rate-driven downside. Here are the most notable European movers:

- Abrdn shares rise as much as 5.7% after the investment company reported profit ahead of estimates and an improvement in flows during the first half.

- Clariane shares rise as much as 16%, the most in a month, after the nursing home operator reaffirmed its organic revenue forecast for the year and reported improved free cash flow.

- Adecco shares gain as much as 5.8%, the most in over nine months, after the Swiss staffing company’s revenue undershot forecasts but was seen to have surpassed the trend at peers.

- Zalando shares jump as much as 6.9%, after the online fashion retailer reported second-quarter gross merchandise volume that came ahead of estimates.

- Rational shares rise as much as 5.4% after the German catering appliances maker reported Ebit that beat estimates for the second quarter due to stronger sales.

- IHG shares rise as much as 4.2%, the most intraday since February, after the hotel operator reported first-half earnings that beat estimates.

- Bayer shares climb as much as 1.4% after the German conglomerate reported better-than-expected sales in the second quarter, helped by strong demand for new cancer and kidney drugs.

- YouGov shares jump as much as 23% after it said its full-year results should beat the guidance given back in June, as the company announced plans to cut costs and a new acquisition.

- Oerlikon shares gain as much as 11% after the Swiss chemicals company delivered results for the second quarter ahead of analyst expectations, boosted by a recovery in its Polymer Processing Solutions unit.

- Galenica drops as much as 5.7%, the most in more than two years after the Swiss health care retailer reported a weaker-than-expected 1H24.

- Domino’s Pizza shares drop as much as 7.7%, hitting the lowest intraday level since July 2023, after the UK pizza delivery store operator reported first-half results that Jefferies said pointed to a slow start to the year.

- Rightmove shares fall as much as 7.3% after the real estate portal said a contract with Openrent will terminate in September.

- Travis Perkins shares drop as much as 3.5% after the DIY and building trade supplier cut its profit guidance for the full year.

Earlier, Asian equities rose, helped by bargain hunting after concerns over a hard landing in the US drove a regional benchmark to its worst single-day drop since 2008. The MSCI Asia Pacific Index jumped as much as 4.2%, heading for its best day since November 2022, following a rout of more than 6% on Monday. Japan led the rebound as the yen eased following steep gains against the dollar that drove the nation’s stocks into a bear market. The Topix index closed with a 9.3% gain, the biggest single-day rally since 2008. Regional equities came under the kosh in the previous two sessions as investors fretted over a possible US recession in addition to overheating of the artificial intelligence rally. Meanwhile, the rapid surge in the yen triggered unwinding of carry trades across the globe, weighing on technology stocks.

“The market reaction was a bit extreme yesterday and hence we see this sharp rebound today,” said Rupal Agarwal, Asia quantitative strategist at Sanford C. Bernstein. “I would expect markets to remain volatile and hence would stick to looking for late-cycle defensive exposure through quality or dividend yielding names.”

In addition to Japan, stocks bounced back Tuesday in technology-heavy South Korea and Taiwan. Chinese stocks were mixed even as local brokerages talked up the prospects of the market in the face of a global selloff.

In FX, the yen dropped after rising to its highest level in seven months, taking a breather from the rally stoked by wagers on further Bank of Japan policy tightening. USD/JPY rose as much as 1.5%, after falling to as low as 141.70 on Monday, the lowest since Jan. 2. Leveraged clients who had previously sold spot higher up bought back, according to an Asia-based FX trader. Bloomberg Dollar Spot Index rose 0.3%. The BOJ’s monetary policy tightening last week has triggered a wave of criticism after it helped set off a historic plunge in Japanese stocks and contributed to global market turmoil — likely putting any plans for further interest-rate hikes on ice.

“Volatile financial market conditions, especially rapid JPY appreciation, are lowering the probability of an October-rate hike” by the BOJ, according to an ING note. “The short-term market volatility won’t change the course of the BOJ’s policy normalization, but the pace may be slower than we expect if it continues.”

In rates, US Treasuries fell as the strong demand for haven assets that marked the start of the week waned globally. Treasuries were cheaper by 3bp to 6bp across the curve in a bear-flattening move with intermediates leading the weakness on the day. The 10-year yield is around 3.86% about 7bp cheaper on the day, trailing bunds in the sector by 8bp, gilts by 4bp; belly-led losses flatten 5s30s spread by nearly 4bp while 2s10s is little changed at around -14bp following Monday’s brief disinversion. Investors pivot from haven demand to supply pressure, with first of this week’s three coupon auctions ahead at 1pm New York when the Treasury will hold a 3-Year, $58BN note auction to be followed by 10- and 30-year sales Wednesday and Thursday. WI 3-year yield ~3.81% is roughly 60bp richer than last month’s, which stopped through by 0.8bp.

In commodities, oil held near a seven-month low as a halt in production at Libya’s biggest field refocused attention on the Middle East. Gold steadied after being pulled into Monday’s global rout, when it slumped as some traders cut holdings to cover potential margin calls.

Looking at today’s market calendar, the US economic data slate includes June trade balance at 8:30am. No Fed speakers are scheduled

Market Snapshot

- S&P 500 futures up 0.8% to 5,261.50

- STOXX Europe 600 up 0.5% to 489.66

- MXAP up 3.3% to 171.48

- MXAPJ up 1.2% to 536.84

- Nikkei up 10.2% to 34,675.46

- Topix up 9.3% to 2,434.21

- Hang Seng Index down 0.3% to 16,647.34

- Shanghai Composite up 0.2% to 2,867.28

- Sensex little changed at 78,816.70

- Australia S&P/ASX 200 up 0.4% to 7,680.64

- Kospi up 3.3% to 2,522.15

- German 10Y yield little changed at 2.19%

- Euro down 0.2% to $1.0934

- Brent Futures up 0.2% to $76.49/bbl

- Gold spot down 0.0% to $2,409.98

- US Dollar Index up 0.25% to 102.95

Top Overnight News

- Japan’s government and central bank sought to show a united front and restore calm to financial markets, after the biggest stocks plunge in more than three decades triggered criticism of monetary policy tightening and cast a shadow over efforts to get households to invest their assets. With some pointing fingers at the central bank’s decision to hike rates last week as part of the trigger for the market turmoil seen in the last few days, the government appears to be trying to show it’s standing with the BOJ remains unchanged. BBG

- Japan cash earnings come in ahead of expectations at +4.5% headline (vs. the Street +2.4%) and +1.1% core (vs. the Street -0.9%), placing hawkish pressure on the BOJ (although household spending fell short). RTRS

- Australia’s RBA leaves rates unchanged (as expected) and rules out a near-term cut given ongoing inflation risks. RTRS

- Samsung’s HBM chips being stockpiled by Chinese firms as they worry having availability limited in the future by US restrictions. RTRS

- U.S. central bank policymakers pushed back on Monday against the notion that weaker-than-expected July jobs data means the economy is in recessionary freefall, but also warned that the Federal Reserve will need to cut rates to avoid such an outcome. Many of the latest job report’s details leave „a little more room for confidence that we’re slowing but not falling off a cliff,” San Francisco Fed President Mary Daly said at an event in Hawaii. RTRS

- Monday’s market rout increases both the risks of recession and a more harrowing financial-market accident. But for Federal Reserve officials who laid the groundwork last week to cut rates by a quarter-percentage point at their meeting next month, the outlook would likely need to deteriorate further in the coming weeks to compel a bigger response. WSJ

- A smaller share of US banks reported stricter credit standards in the second quarter, according to the Federal Reserve. The net share of US banks that tightened standards on commercial and industrial loans for mid-sized and large businesses fell to 7.9%, the lowest since 2022, data from a Fed survey of lending officers released Monday showed. That was down from 15.6% in the prior report. BBG

- Nvidia issued a statement regarding Blackwell production concerns and while it doesn’t address them directly, the company notes that Hopper demand is very strong while broad Blackwell sampling has commenced with production on track to ramp in the second half of the year. Marketwatch

- Execs at Boeing and Spirit AeroSystems face a grilling by the NTSB as it tries to uncover any remaining mysteries surrounding the 737 Max 9 that lost a large fuselage panel mid-air in January. BBG

- Fed’s Daly (voter) said risks to Fed mandates are getting in more balance and minds are open to cutting the rate in coming meetings, while she noted concern is that they will deteriorate from the current place of balance in the jobs report but added that they don’t see that right now. Daly said the July jobs report reflected a lot of temporary layoffs and hurricane effect although she noted that if they react to one data point, they would almost always be wrong. Furthermore, Daly said none of the labour market indicators she looks at are flashing red right now but she is monitoring them carefully and said the Fed is prepared to act as it gets more information.

- US Vice President Harris officially won the Democrat presidential nomination.

- Google will appeal a US District Court ruling that it illegally maintained an online search monopoly by paying companies like Apple to make its search engine the default, TechCrunch reports. The decision, a significant defeat for Google, could reshape its business and the internet’s structure.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly positive as the region rebounded from the recent market turmoil – Nikkei futures saw an upside circuit breaker triggered, while the Korea Exchange activated sidecars for the Kospi and Kosdaq after early surges. ASX 200 traded higher albeit within a confined range as participants awaited the latest RBA policy announcement, while the central bank provided no major surprises as it kept rates unchanged and maintained its hawkish tone. Nikkei 225 bounced back aggressively following its largest-ever daily point drop and reclaimed the 34,000 status. Hang Seng and Shanghai Comp. were somewhat lacklustre with the Hong Kong benchmark gave up initial gains, while the mainland lagged after a substantial daily net liquidity drain.

Top Asian News

- Japan’s Top Currency Diplomat Mimura says no comment on market moves; discussed big moves in financial, stock market with BoJ and FSA; government will work closely with BoJ. Share view that Japanese economy is making a moderate recovery. Discussed forex. Closely watching FX moves. Important for currencies to move in stable manner reflective fundamentals. Held meeting as there we big moves in the stock market. Communicating with authorities overseas on recent market moves.

- RBA kept the Cash Rate Target unchanged at 4.35%, as expected, while it reiterated that the Board remains resolute in its determination to return inflation to the target, is not ruling anything in or out, and inflation remains above target which is proving persistent. RBA added that returning inflation to the target is the priority and policy will need to be sufficiently restrictive until the board is confident that inflation is moving sustainably towards the target range. Furthermore, it upped forecasts for GDP, CPI and the Unemployment Rate with forecasts assuming the Cash Rate will be at 4.3% in December 2024, 3.6% in December 2025, and 3.3% in December 2026.

- RBA Governor Bullock says still risks inflation takes too long to return to target; progress on inflation has been slow for a year; need to stay on course with inflation; near-term cut in rates does not align with Board’s thinking. Board did consider a rate rise. Cut is not on the near-term agenda

Markets found some reprieve following yesterday’s hefty selling, Euro Stoxx 50 U/C; action which was led by a substantial rebound in APAC trade that saw the Nikkei 225 close with gains of over 10%, though not quite paring all of Monday’s record move lower. However, across the European session this strength has waned with European bourses now flat/lower; a paring which has occurred without a fresh fundamental driver. Sectors were primarily in the green, but are becoming increasingly mixed; Tech outperforms as it rebounds with Deutsche Bank also upgrading the European sector while Banks come in a close second place as they trim recent rate-driven downside. FTSE 100 -0.3% is the relative laggard, hit by pressure in defensive large-caps and as the housing sector slumps after housebuilder updates, remains afloat overall due to its banking exposure. Stateside, futures in the green (ES +0.5%, NQ +0.6%) with the narrative the same as the above after the better-than-expected ISM Services began a rebound which looks set to continue. Numerous key earnings ahead incl. Caterpillar, Uber & more.

Top European News

- UK Chancellor Reeves said she wants to strengthen and deepen trade ties with the US and noted that the tax burden in the UK is too high, according to an interview with Bloomberg.

- UK Chancellor Reeves left the door open to higher borrowing to tackle the UK ‘fiscal hole’, according to FT.

FX

- DXY is managing to post modest intraday gains following yesterday’s choppy session, today’s range currently 102.69-103.09, which is well within yesterday’s 102.15-103.21 parameter.

- Upside which comes at the expense of GBP, EUR and mostly notable the JPY. Which are down to lows of 1.2700, 1.0908 respectively and USD/JPY as high as 146.36.

- Though, much of that initial JPY-pressure has pared after the morning’s meeting with MOF, FSA & BoJ officials did not include anything particularly pertinent in the readout.

- Antipodeans diverge; AUD leads after a hawkish RBA hold with the upside extending a touch as the Governor highlighted that a hike was considered.

- PBoC set USD/CNY mid-point at 7.1318 vs exp. 7.1454 (prev. 7.1345).

Fixed Income

- Core benchmarks under modest pressure with Bunds holding just under the 135.00 mark having spent much of the session sub-134.74 open. Briefly extended to a 135.12 peak, seemingly as crude slipped a touch before settling and then climbing once more post EZ Retail Sales & supply.

- A similar narrative for Gilts but with upside for the UK benchmark coming after a strong 2043 DMO tap, which came in better than the stellar prior; an auction which lifted the benchmark more convincingly back above the 100.00 handle.

- USTs holding just off 113-12 lows, which mark a new base for the week but markedly above Friday’s 112-21 base. As such, market pricing has shifted to no longer entirely price in a 50bp cut in September, with the odds of that back down to circa. 75%.

- US 3yr supply the afternoon highlight, and while USTs are at WTD lows it remains to be seen if this factors as concession after the moves on Friday/Monday

- UK sells GBP 2bln 4.75% 2043 Gilt: b/c 3.37x (prev. 3.29x), average yield 4.372% (prev. 4.519%) & tail 0.2bps (prev. 0.1bps)

- Germany sells EUR 3.284bln vs exp. EUR 4bln 2.50% 2029 Bobl: b/c 1.9x (prev. 2.0x), average yield 2.09% (prev. 2.39%) & retention 17.9% (prev. 18.4%)

Commodities

- Crude benchmarks have an underlying positive bias, but are off best levels. A bias which was driven by the overall recovery in sentiment and after bullish remarks from the Aramco CEO re. oil demand.

- Precious metals diverge a touch, XAU firmer but contained at its 21-DMA of USD 2412/oz while XAG slips.

- Base metals are mixed with specifics light and the bounce from yesterday’s downside being somewhat offset for the metals by the creeping USD strength.

- Venezuela’s Attorney General is to open a criminal investigation against opposition leaders Machado and Gonzalez.

- „Aramco President to Arabian Business: Strong demand returns to market fundamentals coinciding with the entry of the driving season…We expect oil demand to increase in the coming months”, via Al Arabiya. Adds, „Strong oil demand from China may continue during the second half of 2024”. Expects global oil demand of 104.7mln BPD in 2024 (vs 104.5mln in OPEC July MOMR), seeing more plans to replenish strategic inventories which will aid healthy demand. In July and early August, saw growth in jet-fuel demand and significant growth in China.

- „Iran, Saudi Arabia discuss expansion of bilateral ties”, according to IRNA.

Geopolitics

- US President Biden and VP Harris were told by the national security team it is unclear when Iran and Hezbollah are likely to launch an attack against Israel and the specifics of such an attack, according to a US official.

- „Chairman of Iran’s National Security and Foreign Policy Committee Describes Haniyeh’s Assassination in Tehran as a Declaration of War”, according to Sky News Arabia.

- US officials said US President Biden was informed of the expectation of a scenario for two waves of attacks, one of which is from Iran and another from Hezbollah. However, it is unclear to US intelligence who will attack first or the nature of the attack, while intelligence indicates that Iran and Hezbollah have not yet decided what exactly they want to do, according to Axios.

- US Secretary of State Blinken said the Middle East is at a critical moment and all parties must refrain from escalation, while it is critical that they break this cycle by reaching a Gaza ceasefire and parties should not look for a reason to delay or say no.

- US Secretary of State Blinken spoke to his Egyptian counterpart and Qatar’s PM on Middle East tensions, while Blinken delivered a consistent message to refrain from escalation and calm tensions in the Middle East. Furthermore, Egypt’s Foreign Minister called on his Blinken to pressure Israel to seriously engage in ceasefire talks in the Gaza Strip.

- Palestinian President Abbas said the killing of Hamas leader Haniyeh intended to prolong the conflict in Gaza, while it was also reported that Abbas is to visit Russia on August 12th-14th, according to RIA.

- Russia has started delivering advanced radars and air-defence equipment to Iran as the country prepares for a possible war with Israel, according to two Iranian officials familiar with the planning cited by NYT.

- Several US personnel were injured in a rocket attack on a base housing US troops in Iraq, according to three officials cited by Reuters. It was later reported that US Defence Secretary Austin spoke with Israeli Defence Minister Gallant on Monday and they agreed that the Iran-aligned militia attack on US forces stationed in Iraq marked a dangerous escalation.

- Explosions were heard in the Ukrainian capital of Kyiv after air raid sirens sounded, according to Reuters.

US Event Calendar

- 08:30: June Trade Balance, est. -$72.5b, prior -$75.1b

Tyler Durden

Tue, 08/06/2024 – 08:09

{kind=link}