We Need To Talk About Recession Risk Again

Authored by Simon White, Bloomberg macro strategist,

It’s time once more to increase vigilance for a US recession.

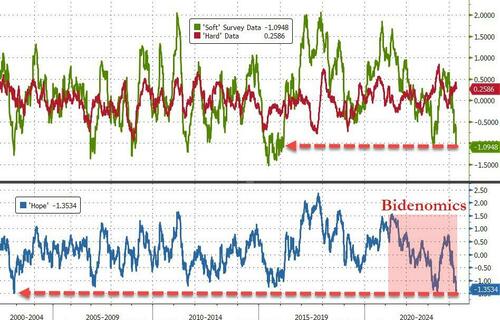

Soft, survey data is starting to deteriorate, while hard data is already fragile. Expectations of a downturn are currently low, but they could quickly swing higher.

Stocks – which experience their worst drawdowns in recessions – are not priced for such an outcome, while yields are biased lower in the coming months.

S curves are nature’s approximation of a binary on-off switch. They pop up in all sorts of places, from neurons in the brain to the progression of diseases, and from population growth to the adoption of new technologies. They also describe how recessions evolve.

Economies are typically believed to develop in a linear fashion, from a non-recessionary to a recessionary state. But instead they do so in a highly non-linear way, with recessions often happening abruptly. Downturns have either a low risk of occurring in the next 3-4 months, or a high risk, but rarely anything in between – much like the shape of an S as depicted below.

That is why most standard recession models don’t make a lot of sense, as they assume recession risk can evolve smoothly. But it is essentially meaningless to talk of the likelihood of a recession rising from, say, 45% to 50%, when we acknowledge their regime-shift nature.

Just now we are at the bottom-left hand side of the S, with a low risk of an imminent recession. But the data has evolved in the last few weeks to suggest we could soon move to the right and on to the steep upward section of the curve – meaning the probability could quickly climb much higher. If so that would make a recession more likely than not over the next 3-4 months.

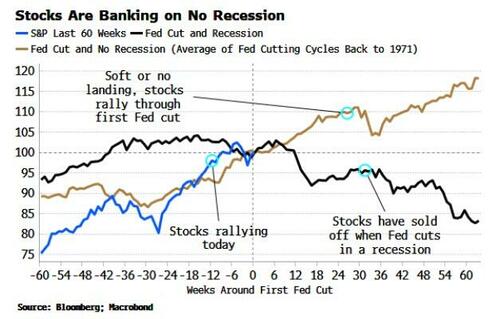

Stocks are expecting a soft or no landing. They are currently behaving in a way consistent with the Fed’s first rate cut — the most likely move if it changes rates this year — occurring in the absence of a recession. However, rate cuts that happen when there is a slump have historically led to a much worse outcome for equities — both before and after the recession — than currently priced (white line in chart below).

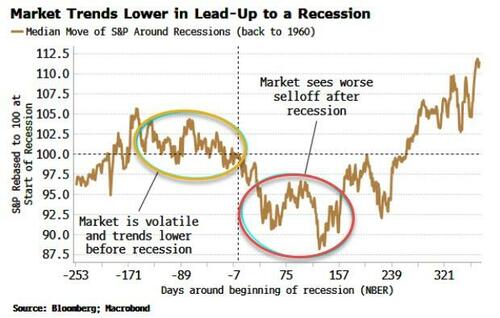

Six months ago I wrote that a US recession was unlikely through most of 2024. That could still end up being the case, but if we are shifting along the S curve, then investors should be prepared for an environment that could quickly look more recessionary, even if an actual downturn doesn’t arrive for another six months. Remember: stocks sell off before the onset of a recession, and even longer before the NBER finally announces the economy is in one.

The upgrading of recession risk has been prompted by the weakening in soft data in recent weeks, coinciding with hard data that remains fragile.

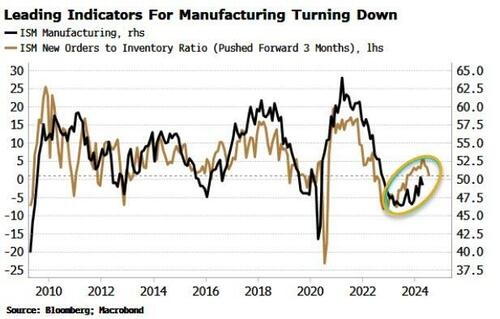

The manufacturing ISM is one of the single-most important data points for the economic and stock outlook.

The headline survey dropped below 50 in April. It is led by the new orders-to-inventory ratio, which is turning lower and slipped below the important level of one, where orders are expected to be just enough to match inventory.

It was the rise in this ratio, along with other indicators, that fed the view last year that the US was likely to avoid a recession for a while yet.

Yet as much as it’s unhelpful to be a perma-bear and constantly expect a recession, it also doesn’t make sense to assume there will be no recession at all. As I have described, one can only have a reasonably accurate view on a downturn occurring over the next 3-4 months, and that view by its nature is likely to change abruptly, not smoothly.

Adding to the difficulty in forecasting recessions, the goods and services economies have fallen out of sync in this cycle. Normally the goods sector leads the rest of the economy into a downturn, which is why so many traditional recession indicators over-emphasized the risk of one last year. But at some point, the economy is likely to resynchronize.

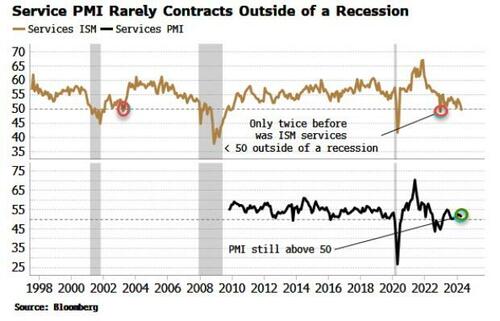

Why it’s particularly important to be more vigilant now is that services might also be notably slowing, as flagged by the services ISM also slipping below 50 in April; it has only done so twice before outside of a recession.

The usual caveats apply. The ISM is quite volatile, and the PMI services survey is still above 50, even though it is also turning lower. But this drop in important soft-data points comes at a time when hard data is showing signs of fragility too.

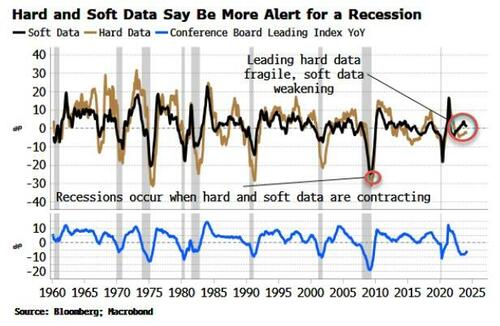

Recessions occur when both hard and soft data are contracting at the same time. Using the inputs to the Conference Board’s Leading Index, growth in leading hard-data has been turning higher, but is still contracting, while leading soft-data is close to slipping into the contraction zone. That would be ominous for recession risk.

Revisions will also be key to monitor. Typically data sees its biggest revisions before and after the occurrence of a recession. Data can be revised lower very quickly which is why recessions can happen faster in revised time than in real time.

What does all this mean practically for investors?

It leaves stocks more vulnerable. As the chart below shows, even though equities see a sharp drawdown after a recession begins (which, remember, we don’t know when that is until after the fact when the NBER announces it), they begin selling off beforehand. Moving to the right of the S curve means more volatile stock prices with a bias lower, even if it does not ultimately mean a full recession-like decline and an end to the bull market.

It also means bond yields are more likely to see some retrenchment in the coming months. But with elevated inflation in the background, bonds are primed to not rally as much as in non-inflationary recessions (see chart below). Moreover, yields are still structurally biased higher due to waning interest in owning USTs at current prices, and an inundation of supply.

Investing is about gauging forward probabilities. The probability of a near-term recession is currently low, but in a month’s time it could be much higher. That would be a lot of new information asset prices would have to quickly digest. A more nimble investment stance is advised at this trickier part of the cycle.

Tyler Durden

Thu, 05/09/2024 – 12:00

{kind=link}